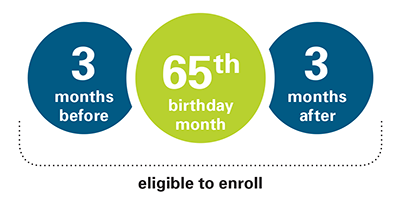

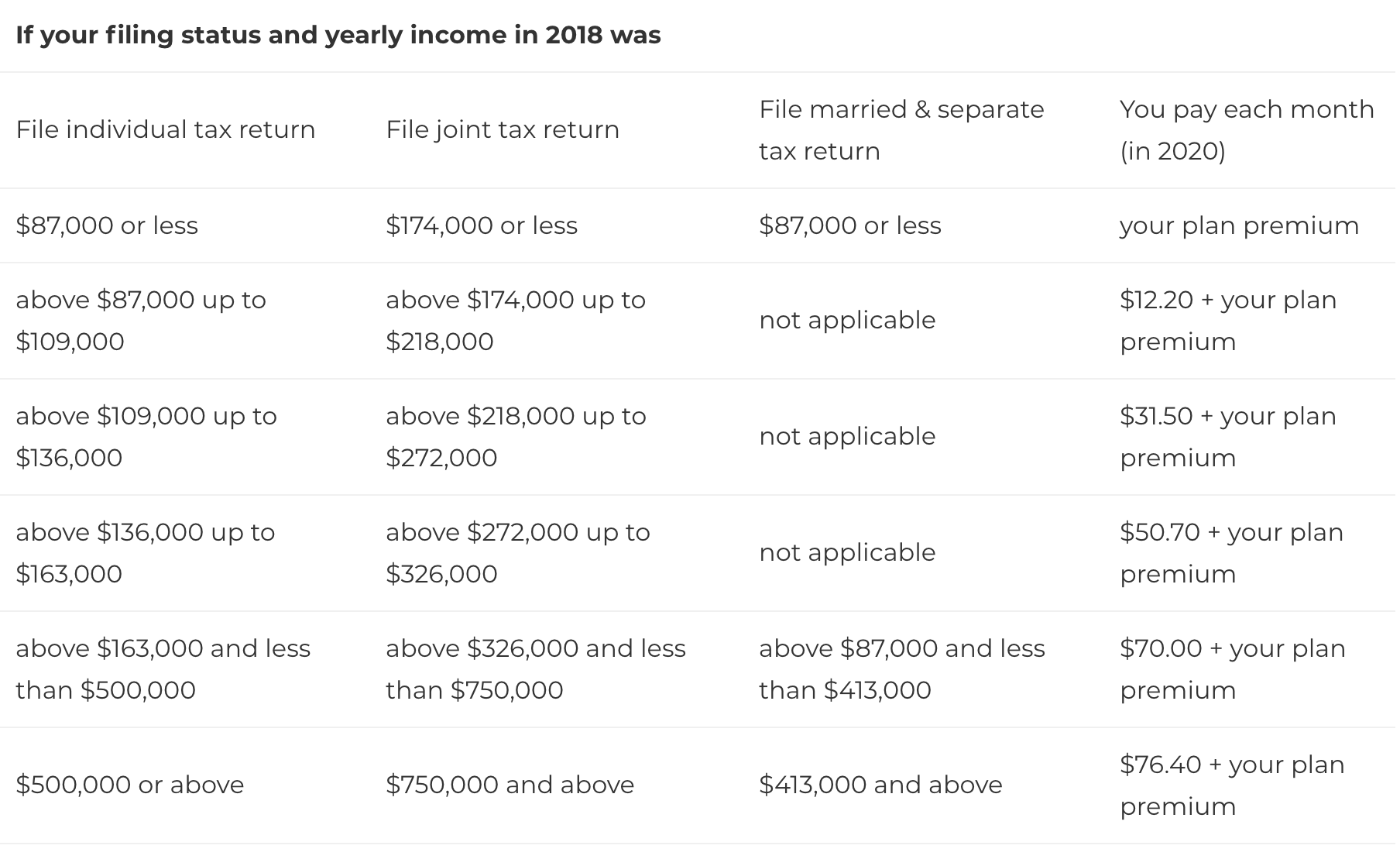

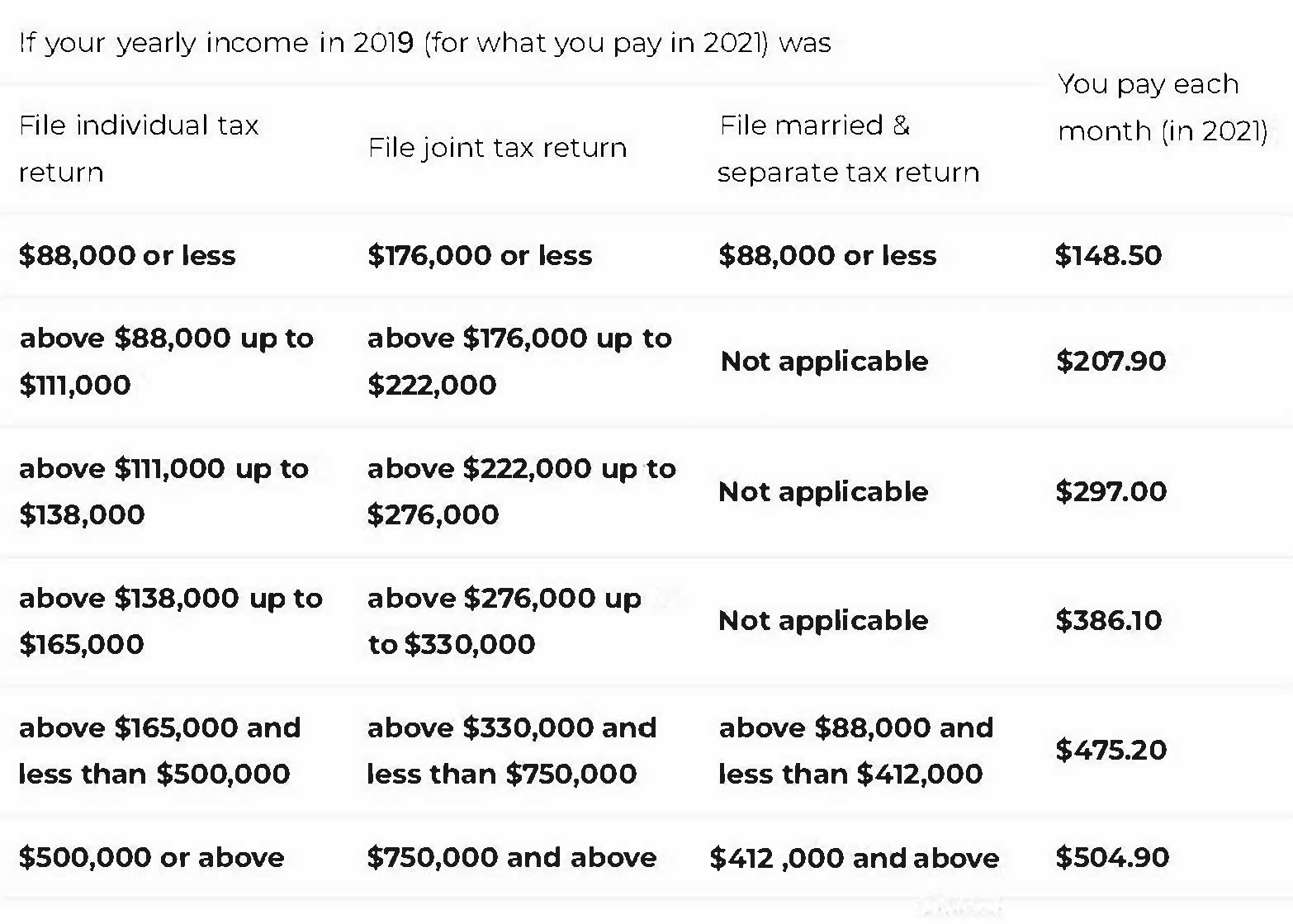

To be eligible for Medicare Part A and Part B, you must be a U.S. citizen or a permanent legal resident for at least five continuous years. Generally, Medicare is available for people age 65 or older, younger people with disabilities and people with End Stage Renal Disease (permanent kidney failure requiring dialysis or transplant), have Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig’s disease. Medicare has two parts, Part A (Hospital Insurance) and Part B (Medicare Insurance). You are eligible for premium-free Part A if you are age 65 or older and you or your spouse worked and paid Medicare taxes for at least 10 years. The standard monthly premium for Medicare Part B enrollees will be $148.50 for 2021. The annual deductible for all Medicare Part B beneficiaries is $203.00 in 2021.

The main coverage options include:

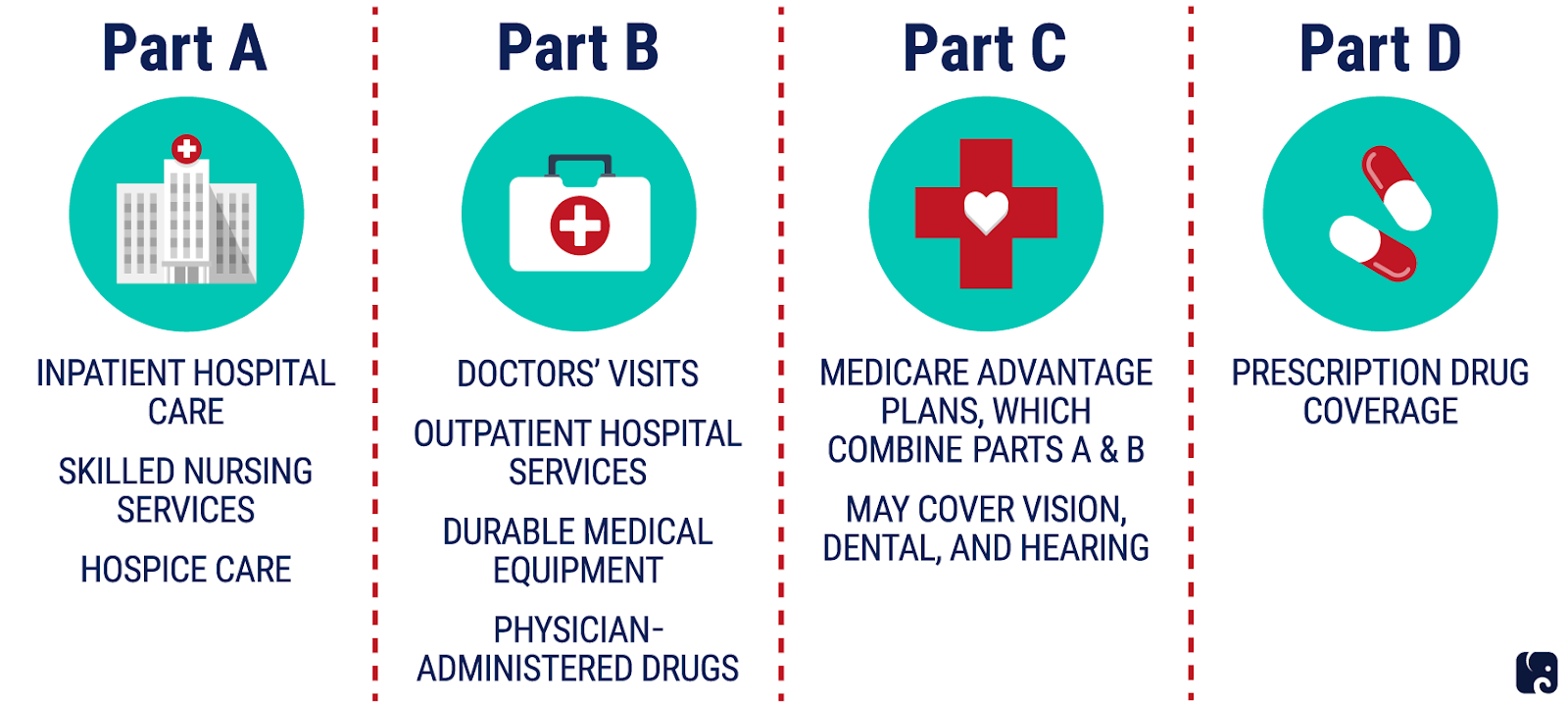

- Original Medicare, which comprises: Medicare Part A – hospital insurance. Medicare Part B – outpatient coverage.

- Original Medicare, which comprises: Medicare Part A – hospital insurance. Medicare Part B – outpatient coverage.

- Medicare Advantage (Part C) A Medicare Advantage Plan (like an HMO or PPO) is another Medicare health plan choice you may have as part of Medicare. Medicare Advantage Plans, sometimes called “Part C” or “MA Plans,” are offered by private companies approved by Medicare. If you join a Medicare Advantage Plan, the plan will provide all of your Part A (Hospital Insurance) and Part B (Medical Insurance) coverage. Medicare Advantage Plans may offer extra coverage, such as vision, hearing, dental, and/or health and wellness programs. Most include Medicare prescription drug coverage (Part D).

- Medicare Advantage (Part C) A Medicare Advantage Plan (like an HMO or PPO) is another Medicare health plan choice you may have as part of Medicare. Medicare Advantage Plans, sometimes called “Part C” or “MA Plans,” are offered by private companies approved by Medicare. If you join a Medicare Advantage Plan, the plan will provide all of your Part A (Hospital Insurance) and Part B (Medical Insurance) coverage. Medicare Advantage Plans may offer extra coverage, such as vision, hearing, dental, and/or health and wellness programs. Most include Medicare prescription drug coverage (Part D).

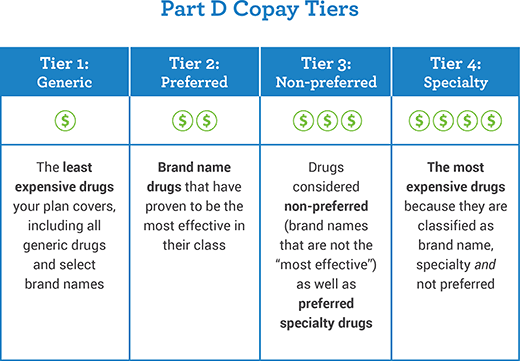

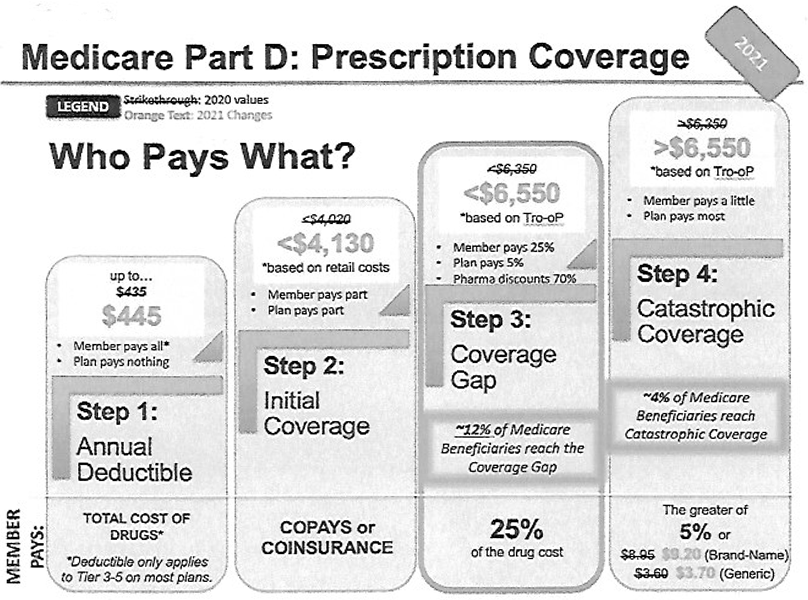

- Medicare Part D – prescription drug coverage.Medicare Part D is simply insurance for your medication needs. You pay a monthly premium to an insurance carrier for your Part D plan. In return, you use the insurance carrier’s network of pharmacies to purchase your prescription medications. … Your Part Dinsurance card will be separate from your Medigap plan.

Medigap – Medicare Supplement insurance. Medigap is extra health insurance that you buy from a private company to pay health care costs not covered by Original Medicare, such as co-payments, deductibles, and health care if you travel outside the U.S. Medigap policies don’t cover long-term care, dental care, vision care, hearing care, vision care, hearing aids, eyeglasses, and private -duty nursing. Most plans do not cover prescription drugs.

| Costs for Part A (Hospital): | What you pay in 2025: |

|---|---|

| Premium | $0 for most people (because they or a spouse paid Medicare taxes long enough while working – generally at least 10 years). If you get Medicare earlier than age 65, you won’t pay a Part A premium. This is sometimes called “premium-free Part A.” If you don’t qualify for premium-free Part A: You might be able to buy it. You’ll pay either $278 or $506 each month for Part A, depending on how long you or your spouse worked and paid Medicare taxes. Remember:

|

| Deductible | $1,600 for each inpatient hospital , before starts to pay. There’s no limit to the number of benefit periods you can have in a year. This means you may pay the deductible more than once in a year. |

| Inpatient stay |

|

| Skilled nursing facility stay |

|

| Home health care | $0 for covered home health care services. 20% of the for durable medical equipment (like wheelchairs, walkers, hospital beds, and other equipment) |

| Hospice care | $0 for covered hospice care services. You may also pay: |

Part B (Medical Insurance) costs

| Part B costs: | What you pay in 2023: |

|---|---|

| Premium | $164.90 each month (or higher depending on your income). The amount can change each year. You’ll pay the premium each month, even if you don’t get any Part B-covered services. You might pay a monthly penalty if you don’t sign up for Part B when you’re first eligible for Medicare (usually when you turn 65). You’ll pay the penalty for as long as you have Part B. The penalty goes up the longer you wait to sign up. Find out how the Part B penalty works and how to avoid it. |

| Deductible | $226, before Original Medicare starts to pay. You pay this deductible once each year. |

| General costs for services (coinsurance) | Usually 20% of the cost for each Medicare-covered service or item after you’ve paid your deductible (and as long as your doctor or health care provider accepts the as full payment – called “accepting assignment”). Find out how assignment affects what you pay. |

| Clinical laboratory services | $0 for covered clinical laboratory services. |

| Home health care |

|

| Inpatient hospital care | 20% of the for most doctor services while you’re a hospital inpatient. |

| Outpatient mental health care |

|

| Partial hospitalization mental health care | After you meet the Part B deductible:

|

| Outpatient hospital care |

|